Non Banking Financial Companies (NBFC) Grading

An independent and unbiased opinion of an enterprise’s creditworthiness

NBFC Grading

NBFC Overview

NBFC grading is an extensive assessment of the business and financial performance of an NBFC and provide the relative capability of the NBFC to manage its operations in a sustainable manner.

NBFCs form an integral part of the Indian financial system

Reaching out credit to the unbanked segments of society, especially to the micro, small and medium enterprises

(MSMEs) and entrepreneurs.

Ground-level understanding of their customers’ profile and their credit needs gives them an edge over banks

Gaining market share in urban and semi-urban areas on account of customer oriented product innovation and superior customer service

Lesser turn-around time (TAT) compared to banks enables NBFCs to establish a strong market presence.

Broadly classified into 11 different categories of NBFCs such as asset finance companies, gold loan companies, and so on.

About the product

NBFCs complement the mainstream banking system. Borrowers reach out to NBFCs on account of their quicker decision making, minimal documentation, swift services and flexibility.

However, given the nature of their business, they cater to the market which is inherently considered a higher risk by the bank. Hence for lenders/investors to take informed decisions, there is a need for such NBFCs, particularly the smaller NBFCs, to be assessed by an external grading agency on a different criteria and scale for NBFCs so as to differentiate the NBFCs better vis-à-vis the conventional debt rating scale where the ratings may be distributed within a narrow range.

SMERA NBFC Grading is an indicator of SMERA’s opinion on the relative capability of the NBFC to manage its microfinance activities in a sustainable manner. With a focus on evaluating the NBFC’s business and financial risks.

SMERA analyzes an NBFCs operating environment, governance structure, management and systems, scalability (in relation to business plans), asset quality, financial profile and credit and risk management policies.

Majority of the registered NBFCs are small and non deposit taking

NBFCs, relatively the smaller, face issue of required credit rating (minimum investment grade)

Majority of the smaller NBFCs are too small to get a rating and hence do not have any rating.

Such smaller NBFCs also have low eligibility limit for raising funds from banks and thus have to depend on getting funding from large NBFCs for bridging the gap of bank funding

Smaller NBFCs may not have effective & diversified product offering or monitoring framework or appropriate risk management policies

Therefore, for lenders/investors to take informed decisions, there is a need for such NBFCs to be compared on a similar platform by an external impartial grading agency and hence the need for grading of NFCs. The NBFC grading has a specific scale for NBFCs so as to differentiate the NBFCs better vis-à-vis the conventional debt rating scale where the ratings may be distributed within a narrow range.

SMERA NBFC Grading is an indicator of SMERA’s opinion on the relative capability of the NBFC to manage its microfinance activities in a sustainable manner. With a focus on evaluating the NBFC’s business and financial risks.

SMERA analyzes an NBFCs operating environment, governance structure, management and systems, scalability (in relation to business plans), asset quality, financial profile and credit and risk management policies.

About the product

Non Banking Financial Companies (NBFCs) play an important role in financial inclusion.

NBFCs complement the mainstream banking system. Given the nature of their business, the cater to the market which is inherently considered a higher risk by the bank. Borrowers reach out to NBFCs on account of their quicker decision making, minimal documentation, swift services and flexibility. NBFC thus price them accordingly to cover the risks.

The success of NBFCs can be attributed to product lines, lower cost, wider and effective reach, strong risk management capabilities to check and control bad debts, and a better understanding of customer segments. Additionally, improving macro-economic conditions, higher credit penetrations, rapid changing consumption themes and disruptive digital trends have influenced NBFC credit growth. Stress in public sector units (PSUs), underlying credit demand, digital disruption for MSMEs and SMEs as well as increased consumption and distribution access and sectors where traditional banks do not lend are major reasons for the switch from traditional banks to NBFCs. But NBFCs also have their problems, specifically the small ones, such as:

- Majority of the registered NBFCs are small and non deposit taking

- NBFCs, relatively the smaller, face issue of required credit rating (minimum investment grade)

- Majority of the smaller NBFCs are too small to get a rating and hence do not have any rating.

- Such smaller NBFCs also have low eligibility limit for raising funds from banks and thus have to depend on getting funding from large NBFCs for bridging the gap of bank funding

- Smaller NBFCs may not have effective & diversified product offering or monitoring framework or appropriate risk management policies

Therefore, for lenders/investors to take informed decisions, there is a need for such NBFCs to be compared on a similar platform by an external impartial grading agency and hence the need for grading of NFCs. The NBFC grading has a specific scale for NBFCs so as to differentiate the NBFCs better vis-à-vis the conventional debt rating scale where the ratings may be distributed within a narrow range.

SMERA NBFC Grading is an indicator of SMERA’s opinion on the relative capability of the NBFC to manage its microfinance activities in a sustainable manner. With a focus on evaluating the NBFC’s business and financial risks.

SMERA analyzes an NBFCs operating environment, governance structure, management and systems, scalability (in relation to business plans), asset quality, financial profile and credit and risk management policies.

Differentiators between Rating & NBFC Grading

Credit Rating

- Credit Rating is an instrument specific exercise which denotes the opinion on probability of default.

- Credit Rating follows a universal scale across all industries, all companies and sizes – ‘AAA’ to ‘D’

- Peer comparison across all industries.

- Assessment includes conduct of the account with lenders, default check, critical analysis of liquidity done to check debt repayment capacity.

Grading

- A comprehensive evaluation on the financial and business strength of the NBFC along with the assessment of code of conduct

- Grading assesses an NBFC’s capacity to carry out its operationsin a sustainable manner and also assesses its code of conduct.

- Grading follows a customize scale for NBFC from small to medium size on a scale of N1 to N8 and C1 to C5

- Selective peer set amongst NBFC of similar size

Credit Rating

- Credit Rating is an instrument specific exercise which denotes the opinion on probability of default.

- Credit Rating follows a universal scale across all industries, all companies and sizes – ‘AAA’ to ‘D’

- Peer comparison across all industries.

- Assessment includes conduct of the account with lenders, default check, critical analysis of liquidity done to check debt repayment capacity.

Grading

- A comprehensive evaluation on the financial and business strength of the NBFC along with the assessment of code of conduct

- Grading assesses an NBFC’s capacity to carry out its operationsin a sustainable manner and also assesses its code of conduct.

- Grading follows a customize scale for NBFC from small to medium size on a scale of N1 to N8 and C1 to C5

- Selective peer set amongst NBFC of similar size

Credit Rating

- Credit Rating is an instrument specific exercise which denotes the opinion on probability of default.

- Credit Rating follows a universal scale across all industries, all companies and sizes – ‘AAA’ to ‘D’

- Peer comparison across all industries.

- Assessment includes conduct of the account with lenders, default check, critical analysis of liquidity done to check debt repayment capacity.

Grading

- A comprehensive evaluation on the financial and business strength of the NBFC along with the assessment of code of conduct

- Grading assesses an NBFC’s capacity to carry out its operationsin a sustainable manner and also assesses its code of conduct.

- Grading follows a customize scale for NBFC from small to medium size on a scale of N1 to N8 and C1 to C5

- Selective peer set amongst NBFC of similar size

Benefits to NBFCs

Offers a SWOT analysis as a tool for internal analysis and initiate improvements measures

Enhances credibility among lenders, investors and borrowers by showcasing certification from an independent rating institution

Benefits to Lenders

- Comprehensive independent evaluation of NBFCs for better credit decision

- Unbiased decision making by independent committee members

- Sharper pricing of loans

- Quicker processing of loans

- Crisp and sharp grading report with analytical insights, SWOT and trends

- Building better quality portfolios for the long run

Benefits to NBFCs

Offers a SWOT analysis as a tool for internal analysis and initiate improvements measures

Enhances credibility among lenders, investors and borrowers

Benefits to Lenders

- Comprehensive independent evaluation of NBFCs for better credit decision

- Crisp and sharp grading report with analytical insights, SWOT and trends

- Quicker processing of loans

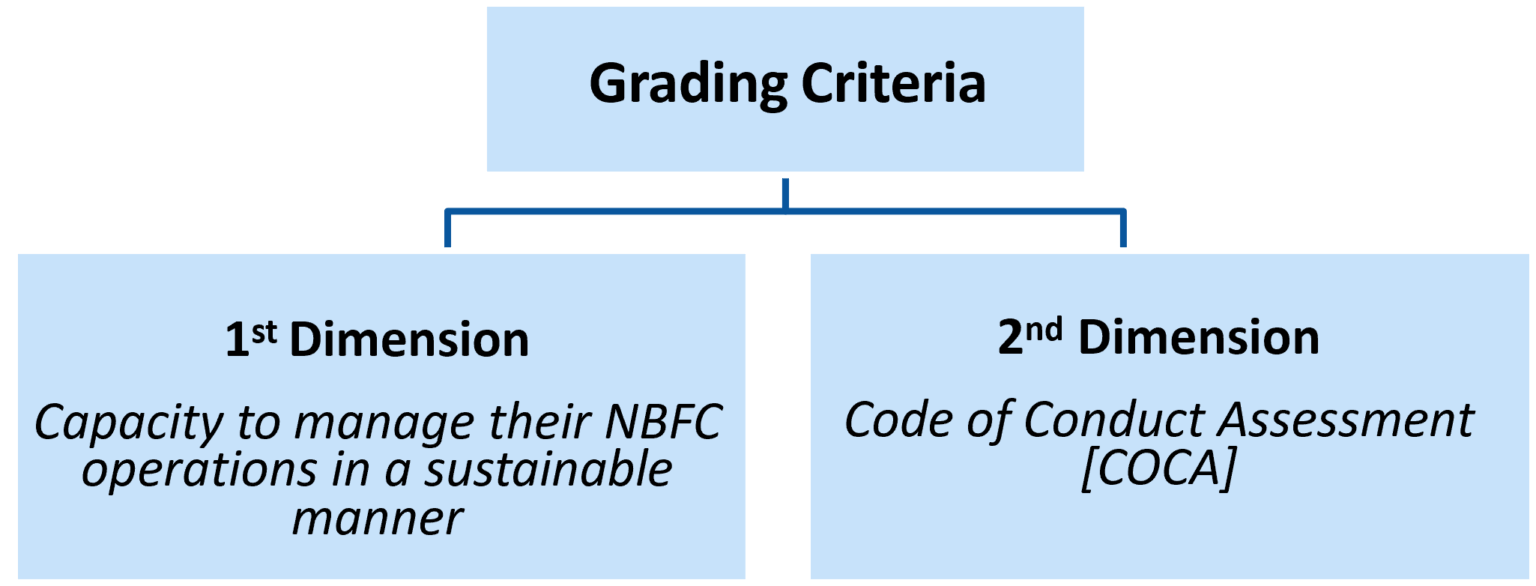

NBFC Grading Criteria

Comprehensive NBFC Grading provides opinion of the Rating Agency on NBFC’s capacity to carry out its NBFC operations in a sustainable manner and its assessment of code of conduct. The assessment of the small NBFCs shall be based on two broad dimensions:

NBFC Capacity Assessment shall be been done on the dimensions of Capital Adequacy, Earning profile, Asset Quality , Management strength and Risk Management Systems.

Assessment on conduct shall be done on the indicators pertaining to Corporate governance, Board Functioning and Strength, Management structure, Transparency and Customer feedback

- NBFC Capacity Assessment shall be been done on the dimensions of Capital Adequacy, Earning profile, Asset Quality , Management strength and Risk Management Systems.

- Assessment on conduct shall be done on the indicators pertaining to Corporate governance, Board Functioning and Strength, Management structure, Transparency and Customer feedback

Management Profile

- Organization Structure

- Profile and credentials of the promoters/ management team

- Integrity & Governance systems

- Business structure

- Vision, mission and future strategy

- Corporate Governance

- Integrity

- Risk Appetite

Quality of Business Model

- Asset class

- Industry Segment

- Break even period, process to control the credit and opex cost

- AUM /Cumulative Loan Disbursed

- Portfolio Seasonality

- Average ticket size

- Geographical Coverage

- Outreach

- Years of Existence

Strength of Operations

- No. of Employees

- No. of Branches

- AUM per employee

- Portfolio Seasonality

- Loan Appraisal Process, Monitoring and Recovery Mechanism

- IT Infrastructure and Management Information System (MIS)

- Asset Quality (Portfolio Ageing)

- Incremental borrowing rate v/s incremental yield on portfolio

Financials Quality

- Resource Profile (Equity and Debt Mix)

- Earnings Quality and Profitability

- Capital Adequacy (CRAR)

- Asset Quality (provisions and write-offs)

- Net worth (Entity + Promoter)

- Accounting Quality

- Liquidity / Asset Liability Management

- Disclosure in financial statements

Code of Conduct – 2nd Dimention

- Management Structure

- Board Structure and Functioning

- Board Compensation

- Board Independence

- Financial Audit & Control

- Management Compensation

- Community support & development

- Data privacy and security

- Employment quality

- Audit committee functioning

- Shareholders rights

Management Profile

- Organization Structure

- Profile and credentials of the promoters/ management team

- Integrity & Governance systems

- Business structure

- Vision, mission and future strategy

- Corporate Governance

- Integrity

- Risk Appetite

Quality of Business Model

- Asset class

- Industry Segment

- Break even period, process to control the credit and opex cost

- AUM /Cumulative Loan Disbursed

- Portfolio Seasonality

- Average ticket size

- Geographical Coverage

- Outreach

- Years of Existence

Strength of Operations

- No. of Employees

- No. of Branches

- AUM per employee

- Portfolio Seasonality

- Loan Appraisal Process, Monitoring and Recovery Mechanism

- IT Infrastructure and Management Information System (MIS)

- Asset Quality (Portfolio Ageing)

- Incremental borrowing rate v/s incremental yield on portfolio

Financials Quality

- Resource Profile (Equity and Debt Mix)

- Earnings Quality and Profitability

- Capital Adequacy (CRAR)

- Asset Quality (provisions and write-offs)

- Net worth (Entity + Promoter)

- Accounting Quality

- Liquidity / Asset Liability Management

- Disclosure in financial statements

Code of Conduct – 2nd Dimension

Evaluation methodology

- Management Structure

- Board Structure and Functioning

- Board Compensation

- Board Independence

- Financial Audit & Control

- Management Compensation

- Community support & development

- Data privacy and security

- Employment quality

- Audit committee functioning

- Shareholders rights

Grading Parameters & Methodology

Management

Business Model

Operational Strength

Financial Quality

Capacity to manage their NBFC operations in a sustainable manner

1st Dimension

The SME Credit Rating Methodology includes a rigorous check of multiple risk factors. This provides an in-depth view of the rated enterprise and an accurate report to Buyers, Bankers and SMEs.

Code of Conduct

COCA

2nd Dimension

Grading Parameters & Methodology

Management

Business Model

Operational Strength

Financial Quality

Code of Conduct

1st Dimension

2nd Dimension

Grading Parameters & Methodology

Management

Business Model

Operational Strength

Financial Quality

1st Dimension

Code of Conduct

2nd Dimension

Grading Parameters & Methodology

Capacity to manage their NBFC operations in a sustainable manner

1st Dimension

Management

Business Model

Operational Strength

Financial Quality

COCA

2nd Dimension

Code of Conduct

Grading Parameters & Methodology

Management

Business Model

Operational Strength

Financial Quality

Capacity to manage their NBFC operations in a sustainable manner

1st Dimension

Code of Conduct

COCA

2nd Dimension

NBFC Grading Process

1

Receipt of grading request from NBFC

2

Submission of required information and documents by NBFC

3

Detailed analysis of financial and operational performance by SMERA analyst

4

Management Discussion / Site visit conducted by SMERA team

5

Report preparation by the analyst

6

Assignment of Grading by the committee

7

Dissemination of Grading to the client

NBFC Grading Process

1

Receipt of grading request from NBFC

2

Submission of required information and documents by NBFC

3

Detailed analysis of financial and operational performance by SMERA analyst

4

Management Discussion/ Site visit conducted by SMERA team

5

Report preparation by the analyst

6

Assignment of Grading by the committee

7

Dissemination of Grading to the client

Grading Scale

N 1

Highest capacity of the NBFC to manage its operations in a sustainable manner

N 2

High capacity of the NBFC to manage its operations in a sustainable manner

N 3

Above Average capacity of the NBFC to manage its operations in a sustainable manner

N 4

Average capacity of the NBFC to manage its operations in a sustainable manner

N 5

Below Average capacity of the NBFC to manage its operations in a sustainable manner

N 6

Low capacity of the NBFC to manage its operations in a sustainable manner

N 7

Very Low capacity of the NBFC to manage its operations in a sustainable manner

N 8

Lowest capacity of the NBFC to manage its operations in a sustainable manner

Note: The final grading is on 8 x 5 matrix combining both the dimensions