Real Estate Grading

An independent and unbiased opinion of an enterprise’s creditworthiness

Real Estate Grading

Real Estate Project (REP) Grading

- Real Estate Project (REP) Grading is an independent assessment of a real estate project by SMERA.

- The real estate grading addresses two critical needs in the sector:

- improved transparency

- objective benchmarking of projects

- Helps buyers identify quality projects within their city

Real Estate Developer (RED) Grading

- Real Estate Developer (RED) assesses a real estate developer’s capability to execute a project as per specified quality standard and complete project within the stipulated schedule.

- The key parameters assessed by:

- track record

- organizational strength

- financial strength. The developer’s

- Capability is benchmarked across other developers in India

Real Estate Project Grading

- Real Estate Project (REP) Grading is an independent assessment of a real estate project by SMERA.

- The real estate grading addresses two critical needs in the sector:

- improved transparency

- objective benchmarking of projects

- Helps buyers identify quality projects within their city

Real Estate Developer Grading

- Real Estate Developer (RED) assesses a real estate developer’s capability to execute a project as per specified quality standard and complete project within the stipulated schedule.

- The key parameters assessed by:

- track record

- organizational strength

- financial strength.

- The developer’s capability is benchmarked across other developers in India

Rating Criteria

Industry Risk Evaluation

The real estate sector is cyclical having direct linkage to macroeconomic scenario, interest rates and income levels. Apart from being cyclical, the sector is also highly fragmented, capital intensive and marred by transparency issues. Risks and uncertainties occurred in all real estate development projects. Risks can strongly influence to each project stages from the project conceptualization, project feasibility analysis, design and planning, bidding and tendering, construction and execution, and handover stage. Real estate properties, just like any other financial asset, constitute investment goods; thus, their acquisition or development involves initial monetary outflows that will only subsequently generate positive cash flows. Nevertheless, future cash flows are uncertain for both their timing and their amount. It is to this variability of possible results that the concept of risk is related. However, the real estate market is not unitary, its knowledge is imperfect, it is cyclical and segmented. It is, thus, an atypical market, and imperfect. As such, the development of techniques for risk assessment of a real estate operation has to face particular difficulties. The development of a property is a long and complex operation that involves numerous subjects; for this reason, it is perpetually threatened by a great variety of risks.

Management Risk Evaluation

Management Evaluation

A developer with an understanding of local area nuances, established brand image in the area of operations, demonstrated track record of quality construction and timely delivery has a competitive advantage. Developers that have been through various business cycles are generally better placed when compared to peers with limited experience.

SMERA Gradings takes cognizance of resourcefulness of the management/promoters, financial strength of the group, and involvement of the group in other business segments. The grading exercise reviews the accounting policies, notes to accounts, contingent liabilities/off balance sheet items, auditor qualifications, etc., to analyze if there is any material impact on the financial capability of the developer. Furthermore, RERA website is also viewed to understand if there are any critical observations against the developer.

Experience of developer/management in real estate development

The experienced top management and promoters in the main line of business can steer the rated entity to achieve its stated goals. They are equipped to resolve the challenges and take critical decisions to achieve the desired success.

Real estate space developed by the group in the past

Completed real estate projects in the past indicate the operational level expertise of the promoters. Significant scale of development undertaken in the past entails better experience of the developer in terms of execution.

SMERA Gradings places emphasis on various details of the past projects such as scale, location, types of projects undertaken (villa, gated communities, commercial spaces, etc.), to better understand the experience of the developer in the past.

Constitution of the entity and complex group structure

Constitution of an entity determines the levels of disclosure, transparency and the legal comfort that may be derived by the various stakeholders. The company having high number of sister concerns in the form of special purpose vehicles and an inter-corporate dealing requires detailed analysis.

Group Support

In a typical group structure where real estate projects are being executed through SPVs, such SPVs are usually analyzed on a standalone level. However, with high level of financial and operational linkages between various real estate entities of the group, SMERA Gradings generally attempts to understand the risks at group level. Accordingly, financials, including cash flow details and operational details of other group entities are generally assessed on best effort basis.

SMERA Gradings also attempts to assess the level of support extended by parent and is generally factored in the analysis. Hence, in line with SMERA Gradings’ methodology on factoring linkages, gradings of an entity may be adjusted on the basis of credit strength of the parent and strength of linkage between entity and parent company. Extent of notch up/down is, however dependent on various factors as laid out in detail in the methodology on factoring linkages.

Operational Risk Assessment

Diversification

SMERA Gradings considers the project portfolio of developer to evaluate if such portfolio is well diversified in terms of revenue streams, geographical positioning as well as construction stage of the projects and other revenue-sharing models such as asset light models. The developer having mix of projects for sale and leasing is viewed favorably as leasing projects provide consistent cash inflows even in the times of slowdown, while the projects for sale secure funding from customers during the construction phase of the project. This apart, projects being undertaken by the developer in the established micro-markets are viewed favorably.

SMERA Gradings further evaluates presence across multiple geographies/ jurisdictions during the grading analysis. Furthermore, the mix of projects at initial stage and advanced stage ensures consistent cash inflows and exposure to various business cycles.

Asset light models, through joint development agreements (JDA), enable developers to significantly increase the scale of operations without excessively leveraging their balance sheets, while land aggregation on the other hand exposes the developer to considerable investment for the acquisition. Where asset light model reduces the funding pressure thereby reducing strain on the cash flow compared to the projects having land being debt funded, SMERA Gradings also takes note of presence of land bank acquired at historical costs which provides the developer with a competitive advantage in terms of pricing and financial flexibility in terms of sale of land parcels, if required.

Execution, legal and compliance risk

SMERA Gradings considers experience of the developer in the region and the construction contractor associated, stage of execution of the project and status of approvals to analyze project execution risk.

The real estate projects require multiple approvals from various State and Central Government Authorities at various stages of project execution. Delays in getting such approvals often hamper the progress of the projects as per the envisaged schedule. This can impact sales and collection in the projects hampering execution.

Scale of projects under implementation vis-à-vis development track record till date

The scale of ongoing projects is compared with the aggregate scale implemented in the past to assess whether the projects currently being undertaken are not very large compared to the past projects executed by the developer. If the proportion of area under development vis´-a-vis´ to the aggregate area developed till date is comparable, it implies smoother execution of the projects.

The type of projects, viz., affordable, mid segment, luxury is also considered to assess if developers have adequate experience in dealing with different project genres. Furthermore, the existence of tight regulations, volatility in demand, contraction of liquidity from the banks and financial institutions makes it imperative to perform the project-specific analysis. Accordingly, stage of construction, regulatory approvals, sales details and means of funding are evaluated project wise.

Booking Status

Higher booking ratio implies favorable market standing of the project leading to smooth cash inflows. Evaluation of marketing strategy of the developer is thus essential as often the intention is to hold the inventory in order to take advantage of rising prices; however, at the same time huge unsold inventory imparts pressure to sell the inventory at lower prices in order to secure the payments thereby exposing the developers to pricing risk.

For computing booking ratio, percentage of area/ units booked out of launched area/ units is considered. Furthermore, the ratio is analyzed in combination with the construction status as the nascent stage of construction is often linked to higher unsold inventory. Location of the projects, product offering, and price quoted vis-à-vis current market rate, competition from projects in the vicinity are the parameters looked into to determine sales risk. Significant deviation in quoted prices from market prices provides an insight about market standing of the developer.

Quantum of registered units

Higher percentage of registrations (wherever registrations are done at construction stage) out of sold units is positively correlated to lesser number of cancellations and it further indicates high level of confidence of buyers in the project, primarily being end users. SMERA Gradings emphasizes on the track record of cancellations in such cases. The mix of customers into end-users and investors is also assessed as these have bearing on the overall cancellations. Higher proportion of end-users in a project is viewed favorably.

Sales momentum

Good market standing of the developer ensures quick sales velocity and regular cash inflows. The estimated period within which unsold inventory gets converted into sales based on the current sales momentum is also looked into. Lower estimated cycle indicates greater sales velocity or insignificant quantum of unsold units lying with the developer.

Funding structure and collection efficiency

SMERA Gradings looks at the funding mix wherein the proportion of funding through debt, customer advances and promoters’ fund are thoroughly assessed. Higher reliance on customer receipts is generally viewed unfavorably as this could lead to cash flow mismatch and later developer may have to rely on debt/external funding to meet the balance project cost. Reputed developers with favorable market standing of the projects usually receive decent bookings even if the project execution is at initial stage.

The construction of the projects in accordance with the timelines envisaged would ensure timely collection of customer advances by the entity based on construction stage, thereby safeguarding the funding for future construction.

Adequacy of committed receivables

SMERA Gradings focuses on the adequacy of committed customer advances (receivables) from confirmed sales in order to fund the balance cost of the projects under implementation & repayment of outstanding debt. Furthermore, evaluation of cash flow position is undertaken to assess if cash inflows in the projected period are adequate to meet the cash outflows.

Financial Risk Assessment

In view of different accounting methods and principles followed by the entities, it becomes challenging to assess the financial risk by considering the financial statements. As per traditional accounting practice, certain entities followed percentage of completion method while others followed project completion method for revenue recognition. However, with the introduction of Ind AS-115, the real estate entities (on which Ind-AS is applicable) will be required to recognize the revenue on the basis of whether performance obligation is satisfied ‘over time’ or ‘at a point in time’, thus the revenue would be recognized once the company performs all its obligations. Resultantly, timing difference in the completion of various projects would potentially increase the time lag in recognizing the revenue which further impacts the financial position of the entity. The companies with higher proportion of lease income, however, remains less impacted. Thus, greater emphasis is placed on evaluating the cash flow positions of the entity and therefore combination of multiple factors becomes crucial for assessing the financial risk.

Cash Coverage Ratio (CCR)

The real estate inventory requires longer timeframe for selling, thus cash flow management and financial flexibility is of paramount importance for timely servicing of debt obligations. Cash flow adequacy is determined by considering cash flow visibility against committed payments.

SMERA Gradings, while making the assessment, generally considers the cash flow position of the projects covered in the analysis for next few quarters to understand the inflows and outflows of real estate entity. Inflows are usually in the form of project receipts, debt, promoter’s contribution, and support from group companies while outflows include project expenses (construction expenses, finance cost, land cost, administration & marketing expenses), corporate expenses, if any (at consolidated level), and repayment of debt obligations. CCR indicates the level of cushion available to the company in meeting the debt obligations.

SMERA Gradings also evaluates the ratio considering opening cash balance/accumulated surplus to the inflows generated in the projected period. Actual cash flows generated are also compared with the initially projected cash flows and the reasons for shortfalls are scrutinised. The ratio being critical indicator of cash flow position of the entity is sensitized to accommodate various scenarios such as delays in project completion leading to lower cash flows from unsold units, fall in collections from sold units, decline in price of unsold units, increase in finance cost or construction costs, etc.

Availability of Liquid balances

The availability of adequate liquid funds can protect the company against any unprecedented downturn in the economy, impacting cash flows. SMERA Gradings analyzes the percentage of repayments due in the following year being covered by the available unencumbered liquid investments and accordingly evaluates if significant buffer is available to meet the repayments due in subsequent year.

Availability of land bank

The size of available land bank is crucial for the entity as developers often acquire lands in advance at lower cost and use it later for the projects under pipeline which provides flexibility to the entity in pricing the projects. Furthermore, the projects executed on the owned lands generally provide higher margin as compared to the projects where the land sharing rights are acquired. Additionally, the prime location and lower acquisition cost vis-à-vis the current market rates are viewed favorably.

Project funding pattern

The real estate business is capital intensive in nature and the entities require huge capital during various phases of project construction. The development of project initiates with acquisition of land which is more often funded through the promoter’s contribution, while the construction of projects is funded through external sources. The funding pattern (Promoter Funds: Debt: Customer Advances) is a function of the sales momentum of the project and the reputation of the developer.

The developers with better market standing have the ability to achieve higher bookings and thus would place higher reliance on customer advances for funding the balance project cost. While lower sales momentum induces the developer to approach other sources of funding such as debt or unsecured loans from promoters/ group companies. However, extremely higher proportion of external funding through debt or customer advances as against promoter funds could result in substantial leveraging/dependence and thus needs a thorough assessment.

Leverage

As covered earlier, the proportion of external debt often remains low if the competitive position of the entity is strong since the inflows from customer advances are generally adequate enough to meet the project cost. To analyze the debt position, SMERA Gradings looks into the ratio of overall gearing and the results are compared with the peer firms with the similar asset portfolios. Lower ratio implies better financial discipline of the developer and strong ability to withstand economic cycles. The various financial ratios are correlated for analysis and are not seen in isolation.

Conclusion

The grading outcome is ultimately an assessment of the fundamentals and the probabilities of change in the fundamentals. Grading determination is a matter of experienced and holistic judgment based on the relevant quantitative and qualitative factors affecting the credit quality of the issuer. SMERA Gradings analyses each of the above factors and their linkages to arrive at the overall assessment of the credit quality of a real estate entity. SMERA Gradings also considers future estimation of the company’s financials based on past trends and strategies, competition, industry trends, economic condition and other considerations.

SMERA Real Estate Developer/Project Grading

- SMERA shall scrutinize the projects/developer based on the quality of legal documentation, construction-related risks and financial flexibility/viability of the project, besides the background and the track record of the developer

- SMERA REP Grading is based on a 7-point grading scale specific to the respective city of the project, with 7-Star being the highest and 1-Star the lowest. This is city specific grading

- SMERA RED Grading is based on a 5-point grading scale specific to the developer, with Developer Grade (DG) A1 being the highest and A5 the lowest

- As project delay are an intrinsic characteristic to the industry, SMERA shall also give a Delay Tolerance Level (DTL) that shall signify the average delay in no. of months that may occur in the project

- Site visit and discussion with project stakeholders

- Project and financial analysis along with debt repayment capability calculations

- SWOT analysis, project cost and time overrun analysis

- Project report with QR code, badge, grading certificate

- Helps to differentiate your project from competitors in the project location and gives you a competitive advantage

- Offers a SWOT analysis as a tool for internal analysis and initiate improvements measures

- Enhances credibility among customers (mainly home buyers), investors (both individual and institutional) and corporate lessees (in commercial buildings) by showcasing certification from an independent rating institution

- Increases pricing power by establishing the quality perception in the minds of customers

- Increases sales velocity by creating the pull factor for customers

- Star rating can complement the entry strategy by highlighting the developer and project acting as a entry strategy

- Star rating process is similar to project appraisal process of lending agencies and hence can aid in faster processing

- Star rated projects benefit lender and borrowers with initial risk assessment as well as periodic surveillance

Grading Methodology

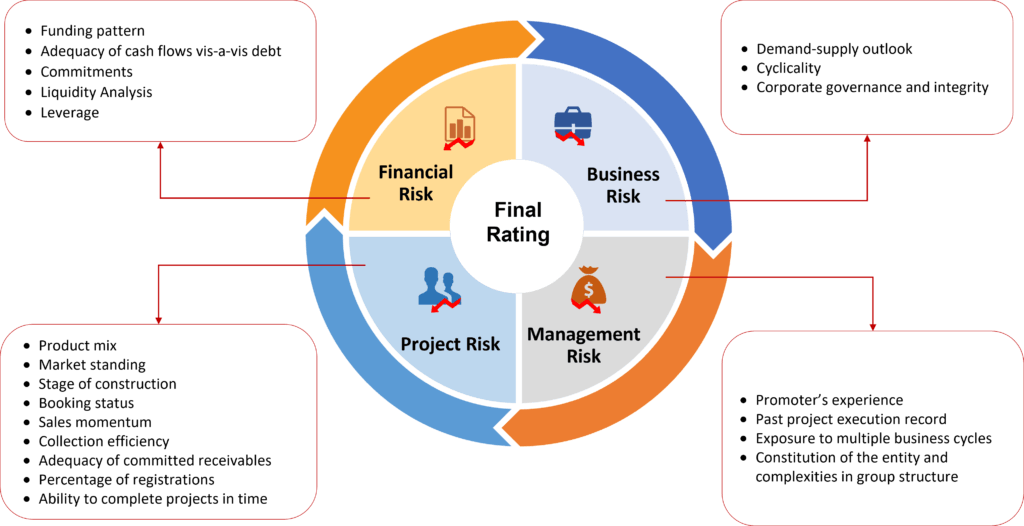

The SME Credit Rating Methodology includes a rigorous check of multiple risk factors. This provides an in-depth view of the rated enterprise and an accurate report to Buyers, Bankers and SMEs.

Financial Risk

• Funding pattern

• Adequacy of cash flows vis-a-vis debt

• Commitments

• Liquidity Analysis

• Leverage

Business Risk

• Demand-supply outlook

• Cyclicality

• Corporate governance and integrity

Management Risk

• Promoter’s experience

• Past project execution record

• Exposure to multiple business cycles

• Constitution of the entity and complexities in group structure

Project Risk

• Product mix

• Market standing

• Stage of construction

• Booking status

• Sales momentum

• Collection efficiency

• Adequacy of committed receivables

• Percentage of registrations

• Ability to complete projects in time

Execution Process

The 6 step Execution Process ensures that each aspect of the enterprise is taken into account, evaluated and measured appropriately.

1

Submission of Information & Documents

2

Site Inspection & Management Discussion

3

Detailed Analysis by Rating Analyst

4

Assignment of Rating by Rating Committee

5

Communication of Rating to the Rated Entity

6

Dissemination of Rating

1

Submission of Information & Documents

2

Site Inspection & Management Discussion

3

Detailed Analysis by Rating Analyst

4

Assignment of Rating by Rating Committee

5

Communication of Rating to the Rated Entity

6

Dissemination of Rating

1

Submission of Information & Documents

2

Site Inspection & Management Discussion

3

Detailed Analysis by Rating Analyst

4

Assignment of Rating by Rating Committee

5

Communication of Rating to the Rated Entity

6

Dissemination of Rating

Delay Tolerance of Real Estate Projects

Real Estate industry and project specifically are exposed to delays arising out of various factors internal or external to the developer of the project. Hence the grading approach offers a more statistical information and objectivity to the buyers and helps them differentiate between projects. SMERA gradings also signifies expected project delays:

Star Grade

Delay in Months

Up to 3 months

6

12

18

24

30

More than 30

Grading Scale

Project Grading

7 ★

Highest likelihood of a project being delivered as per specifications and quality.

Such projects are usually delivered with least delay.

6 ★

Very high likelihood of a project being delivered as per specifications and quality.

Such projects are usually delivered with very low delay.

5 ★

High likelihood of a project being delivered as per specifications and quality.

Such projects are usually delivered with low delay.

4 ★

Above Average likelihood of a project being delivered as per specifications and quality.

Such projects are usually delivered with average delay.

3 ★

Average likelihood of a project being delivered as per specifications and quality.

Such projects are usually delivered with above average delay.

2 ★

Below Average likelihood of a project being delivered as per specifications and quality.

Such projects are usually delivered with high delay.

1 ★

Lowest likelihood of a project being delivered as per specifications and quality.

Such projects are usually delivered with maximum delay.

Developer Grading

DG A1

Excellent

The developer’s ability to execute real estate projects as per specified quality levels within the stipulated time schedule, and to transfer clean title, is excellent.

DG A2

Very Good

The developer’s ability to execute real estate projects as per specified quality levels within the stipulated time schedule, and to transfer clean title, is very good.

DG A3

Good

The developer’s ability to execute real estate projects as per specified quality levels within the stipulated time schedule, and to transfer clean title, is good.

DG A4

Average

The developer’s ability to execute real estate projects as per specified quality levels within the stipulated time schedule, and to transfer clean title, is average.

DG A5

Below Average

The developer’s ability to execute real estate projects as per specified quality levels within the stipulated time schedule, and to transfer clean title, is below average.

Note: SMERA may apply ‘+’ (plus) sign for gradings from ‘DA1’ to ‘DA4’ to reflect comparative standing within the category