MFI GRADING

Microfinance involves providing credit and other financial services and products to the economically challenged to enable them to raise their income levels and living standards. Typically, customers of Microfinance institutions (MFIs) do not have access to banking services and depend on informal sources for their credit requirements.

MFIs fulfil the critical objective of providing financial services to the economically challenged; such services enable clients to meet their credit requirements, fulfil their entrepreneurial ambitions and enhance their economic status. However, microfinance can create a lasting impact in society only if it is provided on a sustainable basis. To make this happen, SMERA offers risk assessment (including MFI grading) and diagnostic services to help MFIs and other constituents in the microfinance industry to measure, mitigate and manage their business and financial risks. Lenders, donors and investors also benefit substantially from SMERA’s inputs because their growing microfinance portfolios demand an intensive, sustained assessment of key monitorable.

CHARACTERISTICS OF MFIs

- The nascent state of the microfinance industry, the world over, and the limited size of MFIs

- Most MFIs either began as non-governmental organisations (NGOs) or were nurtured by NGOs, resulting in a non-commercial orientation

- Most MFIs are not regulated and do not adhere to prudential norms, unlike banks and financial institutions

- Most MFIs have a governance structure of their own

- A number of MFIs are characterised by an absence of capital/equity

- MFIs have distinct lending models that help them maintain asset quality

BENEFITS

Independent third-party opinion

Provides unbiased rating to MFIs, enhances credibility, and also helps adopt good governance policies for sustainability.

Builds confidence with business partners

A good rating provides comfort to lenders, including bankers, financial institutions, NBFCs and collaborators to partner with the related MFIs.

Self-improvement tool

This helps the rated entity to identify areas of improvement and plan for corrective measures.

METHODOLOGY

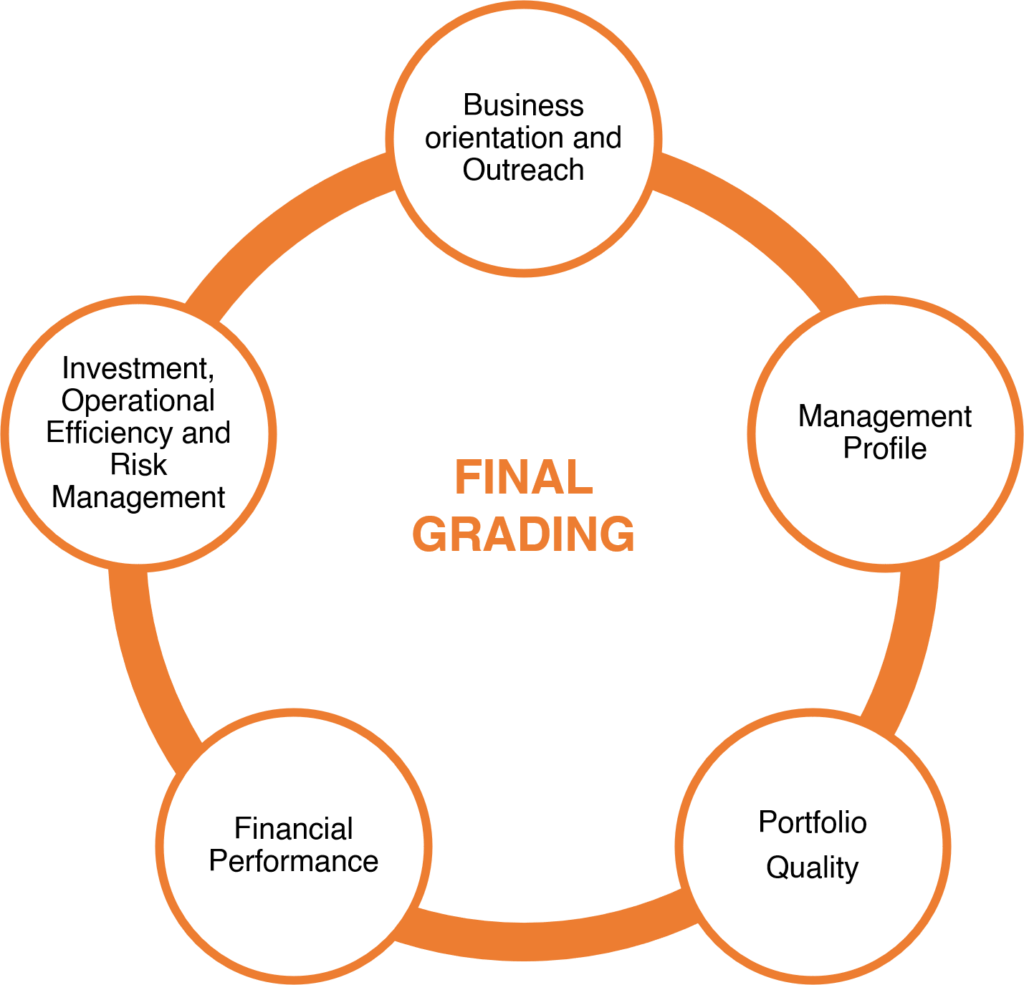

GRADING CRITERIA

- Capital Adequacy & Components of capital

- Portfolio of Risk

- Coverage Ratios, Provision Expense Ratio, Operating Expense Ratio

- Cost of Funds & Cost Per Borrower Return on Assets & Equity

- Operational Cost

- Profitability per Branch & Employee

- Fund Management & Sourcing

- Managing & Sourcing of funds

Microfinance Grading

- Portfolio Diversity

- Market Penetration and Financial Services

- Effective Management of Systems & Processes

- Competency in Interaction with borrowers

- Independent Risk Management Monitoring & Supervision

- Loan Sanction & Disbursal Policies

- Management of credit, Market & Operational Risks

- Management of Legal & Compliance Risks

- Fraud Detection & Reputation & Strategic Risk

- Capital Adequacy & Components of capital

- Portfolio of Risk

- Coverage Ratios, Provision Expense Ratio, Operating Expense Ratio

- Cost of Funds & Cost Per Borrower Return on Assets & Equity

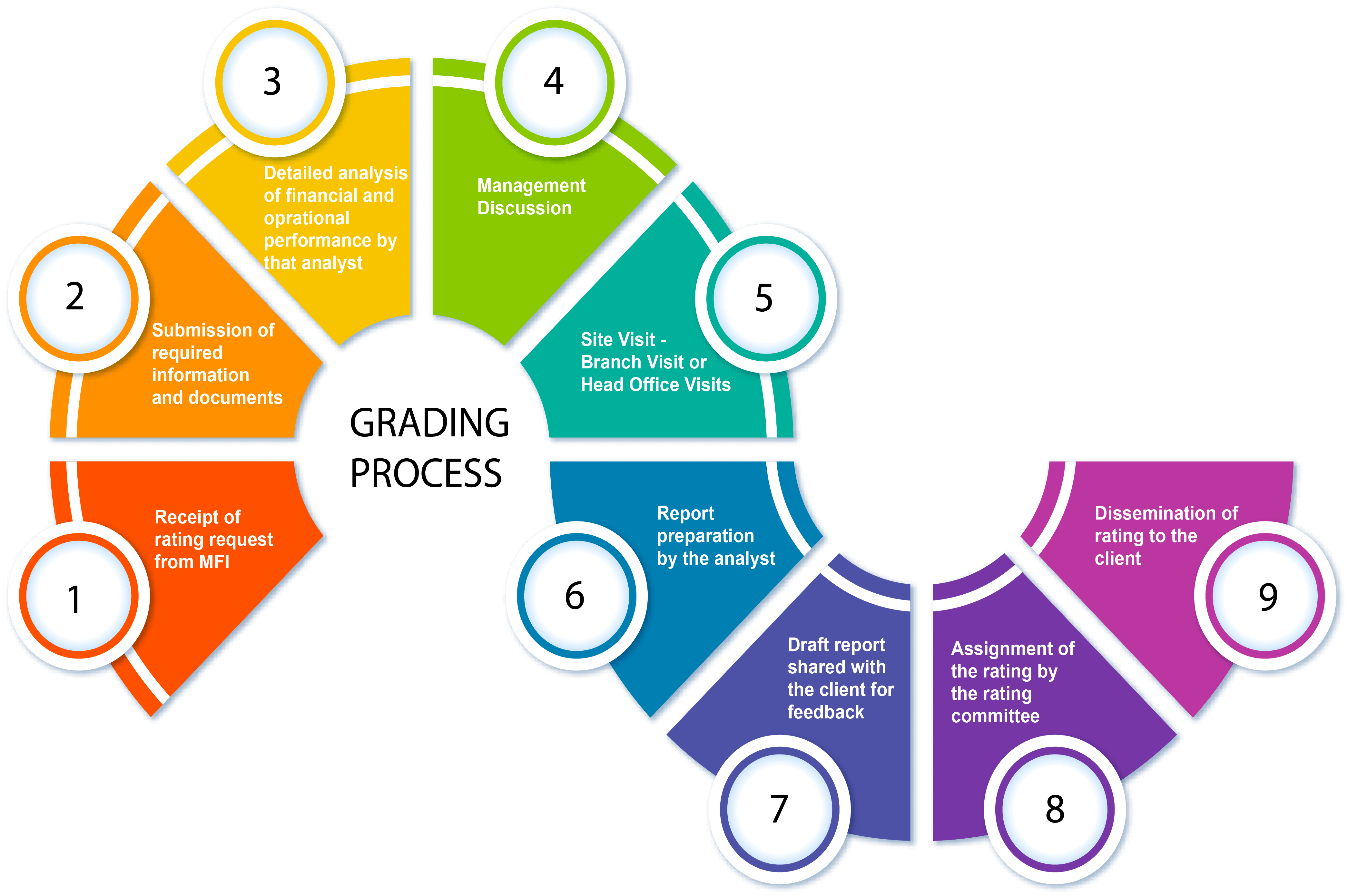

Receipt of rating request from MFI

Submission of required information and documents

Detailed analysis of financial and oprational performance by that analyst

Management Discussion

Site Visit - Branch Visit or Head Office Visits

Report preparation by the analyst

Draft report shared with the client for feedback

Assignment of the rating by the rating committee

Dissemination of rating to the client

GRADING CRITERIA

Management Quality

- Knowledge & Competence Business Strategies Financial & Accounting Polices

- Business Strategies

- Corporate Governance Policies & Processes

- Management Consistency

- Vision & Social impact of the organization

Business Model

- Portfolio Diversity

- Market Penetration and Financial Services

- Effective Management of Systems & Processes

- Competency in Interaction with borrowers

Operational Efficiency

- Operational Cost

- Profitability per Branch & Employee

- Fund Management & Sourcing

- Managing & Sourcing of funds

Risk Management

- Independent Risk Management Monitoring & Supervision

- Loan Sanction & Disbursal Policies

- Management of credit, Market & Operational Risks

- Management of Legal & Compliance Risks

- Fraud Detection & Reputation & Strategic Risk

Financial Performance

- Capital Adequacy & Components of capital

- Portfolio of Risk

- Coverage Ratios, Provision Expense Ratio, Operating Expense Ratio

- Cost of Funds & Cost Per Borrower Return on Assets & Equity

GRADING PROCESS